Fixed liabilities are those long term liabilities which a company has to pay after more than one year. It simply means that these liabilities become due for a business enterprise after one year.

The total figure of these liabilities is used to check the dependency of a firm over its long terms debt instruments. For this purpose, it is used in ‘Debt to equity ratio’, which indicates balance between equity and debt used by a firm to raise funds.

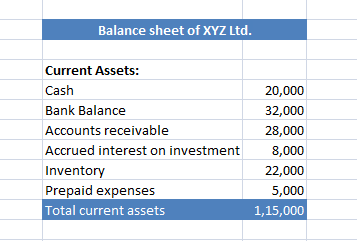

These liabilities are shown on the liability side on a balance sheet.

List of fixed liabilities:

- Debenture

- Bonds

- Mortgages

- Pension obligations

- Lease obligations

- Loans and advances from subsidiaries

- Loans and advances from banks

- Other long term loans and advances.